The CES 2026 chatter about a factory that could churn out 30,000 humanoid robots a year has become a case study in misattribution as much as ambition. The headline is accurate in scope only as a strategic signal, not a near-term plan. Hyundai Motor Group is raising its total U.S. investment to $26 billion across 2025–2028, and a robotics line item sits inside that package. The real fulcrum is what the plant represents for cost, reliability, and scale, not the velocity of Atlas shipments into the wild. In short: a humanoid supplier verticalizing into high-volume manufacturing is the proper lens, and the timing is the secondary question.

From the outset, two facts must be held apart to avoid conflating aspiration with delivery. Atlas production has begun in Boston, and the 2026 run is fully committed to internal and partner pilots. The 30,000-per-year capacity is aspirational and centered on fleet economics at scale, not a turnkey order book for immediate use. The genuine inquiry for operators is not whether a humanoid can do a task, but at what per-unit cost, uptime, and total cost of ownership deploying one beats the alternative at fleet scale. This piece unpacks that distinction and then maps the steps from pilots to a true deployment model.

Why this matters now: the industry faces a labor gap that may justify capex even when capability remains evolving. Deloitte and The Manufacturing Institute project as many as 2.1 million U.S. manufacturing jobs could go unfilled by 2030, with a potential economic cost near $1 trillion. The 30,000-unit plant is a credible increment in supply that targets cost and reliability rather than demonstrating novelty. The challenge for operators is not mythologizing the technology, but tracking concrete metrics that reveal whether the fleet economics work at scale. This analysis follows four lenses—analytics, contrast, cause-and-effect, and expert reconstruction—to separate signal from headline noise.

Analytics perspective: reading the ambition

The core signal is not a promise to replace every worker but a capital-expenditure bet that scale can make humanoids cost-competitive. The numbers are precise in their framing even when the interpretation invites skepticism. Hyundai’s package includes a broad investment envelope, and the robotics line item is a piece of a diversified industrial strategy, not the centerpiece. The shift from capability to cost and reliability hinges on a few critical variables that are visible today only as targets, not confirmed realities.

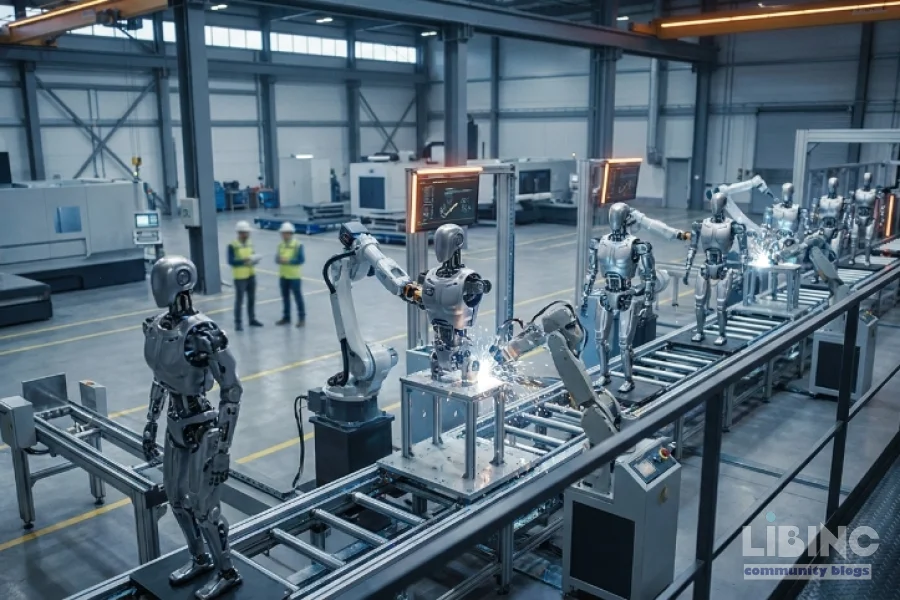

Two operational anchors anchor the analytics: uptime and duty-cycle. The Atlas platform introduced at the Boston headquarters is designed for industrial duty, with autonomous battery swapping and a restricted operating window of roughly 20°C to 40°C. The swapping capability is not a gimmick; it is a mechanism for multi-shift uptime that aims to reduce manual intervention and improve fleet-level availability. The implication for cost modeling is clear: if a humanoid can maintain productive hours across a shift with minimal downtime, the per-unit cost and, ultimately, the total cost of ownership become the levers that unlock CAPEX viability.

Table stakes for cost modeling, therefore, shift away from one-off demonstrations and toward data-based fleet economics. The absence of public per-unit pricing creates a council of uncertainty, but the lack of a published price does not erase the economic logic. If autonomous battery swapping reduces downtime by a meaningful margin, the incremental cost of operating a single unit drops, and a fleet of tens of thousands becomes financially tangible. This is the critical analytics premise: the factory is a cost-lowering engine in waiting, not a demonstration of robotic finesse alone. The key metric to watch is uptime as a duty-cycle enabler and its translation into per-unit cost across 2–3 shifts and beyond.

- Fleet economics: how uptime, duty-cycle, and maintenance costs converge to reduce the cost per task.

- Per-unit cost: the unknown variable whose decline is the practical hinge of the capex argument.

- Autonomous battery swapping: a core uptime enabler rather than a novelty.

From an analytics standpoint, the 30,000-unit plant reads as a capacity commitment aimed at cost and reliability, not a short-term shipping schedule. The gap between a committed 2026 run and a plant designed for tens of thousands is the critical brewing point that operators must monitor. If the fleet economics do not materialize, the plant remains speculative capacity; if they do, the procurement dynamics could shift rapidly toward scalable humanoids as a base-cost component in manufacturing.

Contrasting narratives: what the numbers imply

Two narratives run in parallel around Atlas and Hyundai: a near-term reality of limited, committed production and a longer horizon of industry-wide scale-up. The 2026 Atlas run is already spoken for, with units allocated to Hyundai’s RMAC and Google DeepMind. The rest of the market will see open orders only in 2027. This timing mosaic matters because it defines the difference between pilots in controlled environments and true fleet economics in third-party plants. The contrast is not simply between hardware capability and cost; it is between a capex plan and a real product with an executable price point.

In the near term, the emphasis remains on validation and integration within interior ecosystems. The Atlas iteration has been redesigned for reliability and ease of maintenance, but the actual cost of integration with existing manufacturing lines remains undefined. Operators should be wary of treating 2026 as a proof of purchase. It is better understood as a validation stage that will inform the first credible price signals and the early adopter framework in 2027. The practical consequence is a shift in evaluation criteria: the question is not just whether a humanoid can perform tasks, but whether it can sustain those tasks at a per-unit cost that justifies fleet-scale deployment.

Two diagnostic contrasts emerge from the data. First, the 30,000-unit plant is a capex bet on labor replacement through scale, not a turnkey labor swap in 2026. Second, the existence of a verticalized supplier—humanoid robots as a manufacturing asset—reframes the problem from a software-centric feasibility to a factory-floor uptime and maintenance problem. These contrasts redefine what operators should measure: price visibility, long-term reliability, and the economics of scale across an entire plant portfolio rather than a single prototype line.

- Delivery schedule vs. capacity commitment: pilots this year, fleet-scale potential later.

- Vendor verticalization: hardware, software, and services integrated into high-volume manufacturing.

- Realistic procurement criteria: per-unit cost, uptime, TCO, and fleet readiness.

The takeaway is blunt: even at full build-out, 30,000 units a year remains a rounding error against the broader job shortfall. The real question is whether the cumulative effect on labor costs and throughput justifies the plant's scale. If the per-unit cost and uptime metrics improve as promised, the 30,000-unit target could become a credible productivity lever for manufacturers facing skilled-trade shortages and throughput bottlenecks. If not, the plant exposes how airy aspirational figures can be when set against complex, multi-shift operations and supply-chain realities.

Cause and effect: from pilots to fleet economics

The labor gap is the essential backdrop against which the 30,000-unit plant is framed. Without a sizable improvement in per-unit economics, automation deployments would remain marginal, even with a high-profile partner in Atlas and Hyundai. The causal chain begins with the shortage of skilled labor and ends with a capital-intense attempt to close the gap through volume manufacturing. Each link in that chain must prove itself for the broader hypothesis to hold water.

First, pilots validate capability but do not prove fleet viability. The RMAC and DeepMind collaborations serve as controlled environments where the robot’s learning loop, perception, and manipulation can be refined. The absence of published cost metrics in these pilots means operators must rely on qualitative signals rather than a defensible ROI forecast. The effect is a delay in the onset of real procurement discussions while the business case is sharpened around cost and reliability metrics that directly affect total cost of ownership.

Second, uptime and duty-cycle improvements translate directly into reduced labor costs, but only if the reduction is stable across multi-shift operations. Autonomous battery swapping is a hinge feature; its effectiveness in sustained 24/7 operations remains unproven outside pilots. The implication for fleet economics is simple: if uptime remains patchy, the TCO remains higher than a comparable automation strategy. The 30,000-unit scale is the lever that could turn a marginal improvement in uptime into a meaningful reduction in per-unit cost across the entire fleet.

- Labor replacement vs. labor augmentation: what tasks can humans relinquish, and at what cost?

- Multi-shift uptime: does autonomous swapping deliver continuous productivity?

- ROIC for factory-scale humanoids: when do the capital costs become cash-flow positive?

Finally, the 2.1 million unfilled jobs forecast frames the market as structurally ready for automation, not merely cyclical. The critical implication for operators is not whether humanoids can perform a given task today, but whether cost and reliability will make the fleet a credible alternative to human labor over a multi-year horizon. If the capex signal holds, the 30,000-unit plant becomes a testbed for fleet economics that could redefine commissioning strategies for entire facilities, not just isolated production lines.

Expert reconstruction: watchpoints for deployment

The prudent operator view treats the 30,000-unit ambition as a capital allocation decision that will be resolved through data—not headlines. The near-term milestones are explicit and describe a progression from pilots to early adopter deployments in 2027. Until then, every number remains aspirational, and the real evidence will come from disclosed per-unit costs, uptime data, and the shape of the 2027 order book. Smart operators should anchor planning on tangible signals rather than speculative scale.

There are four practical watchpoints that any deployment case should insist upon before considering scale-up investments:

- Public per-unit cost disclosure: the cost metric that underwrites the entire pro forma, including maintenance and integration.

- Uptime and maintenance metrics: the reliability profile across shifts, with clear downtime budgets and predictive maintenance indicators.

- Total cost of ownership models: a transparent framework covering acquisition, integration, downtime, and support costs over the asset lifetime.

- Fleet economics validation: demonstrable data showing that a multi-unit deployment delivers a meaningful ROI compared with human labor augmentation.

The forward-looking view is not that humanoid robots will instantly displace workers, but that their economics will be credible enough to justify the capital-intensive path to fleet-scale adoption. For operators, the prudent posture is a measured, pilot-informed plan that prioritizes data-driven price discovery and a staged ramp to scale. The factory represents conviction about where the problem now lives—cost and reliability—while actual deployment will be dictated by verifiable performance and a clear path to fleet economics achievable within 2027–2030.

Bottom line: the news is less about Boston Dynamics delivering 30,000 robots this year and more about Hyundai’s determination to turn a humanoid-human-capability frontier into a cost-optimized manufacturing asset. If the per-unit cost, uptime, and TCO data arrive on time and prove favorable, the factory becomes the blueprint for how a hardware-led robotics industry transitions from research platforms to scalable, fleet-based production. Until then, treat the 30,000-unit figure as a capacity bet wrapped in a capex story—an important signal that the market is recalibrating around cost, reliability, and scale.

In that light, the right posture for operators is selective piloting, continuous data collection, and disciplined cost modelling. The 30,000-unit plan may not deliver this year, but it is a meaningful bet on where the industry is headed: a world where humanoids are evaluated the same way as any capital asset, not as a perpetual R&D curiosity.

Notes for readers: The core idea hinges on fleet economics—per-unit cost, uptime, total cost of ownership—rather than a sprint-to-market myth. The milestone dates and unit counts should be treated as directional milestones, not guaranteed outputs.

Closing the practical economics: turning numbers into action

To move from aspiration to real deployments, operators need a transparent framework linking upfront costs, uptime, and maintenance to ROI. The stable lever is scale: a large, continuous fleet that spreads fixed costs and lowers per-unit cost. Below is a compact model and practical scenarios that illustrate how a 2-3 shift operation might approach break-even within a few years.

| Cost Component | Unit Cost USD | Ongoing USD/yr | Downtime Cost USD/yr | 3-yr TCO USD |

|---|---|---|---|---|

| Robot hardware | 28,000 | 3,000 | 9,000 | 67,000 |

| Battery swapping infra (per unit share) | 3,500 | 900 | 3,000 | 18,000 |

| System integration & training | 2,000 | 500 | 1,000 | 6,500 |

| Software updates & support | 0 | 1,200 | 0 | 3,600 |

Key takeaways: uptime, duty-cycle, and maintenance drive the total cost; per-unit cost is the lever that, if driven down, makes fleet-scale deployment feasible.

Operational scenarios show how maintaining high uptime lowers the effective per-task cost, enabling faster ROI on the capital spend.

- Deployment stages

- Pilots 2026-27

- Early adopter deployments 2027-28

- Fleet-scale ramp 2028-2030

- Evaluation criteria

- Public per-unit cost disclosure

- Uptime and maintenance metrics

- Visible fleet ROI

The forward look remains credible: if cost and reliability data materialize, humanoids can become routine assets within industrial workstreams, not just experimental platforms.

Notes: The figures above are directional and meant to illustrate the logic of fleet economics rather than exact forecasts.What does fleet economics mean for humanoid deployment?

Fleet economics is a practical ROI framework that weighs upfront robot costs, ongoing maintenance, and downtime against labor savings and throughput gains across multiple units and years. In practice, operators model per-unit costs, uptime targets, and multi-shift productivity to identify break-even points and scale viability. This lens helps distinguish pilots from deployment-ready plans.

How is per-unit cost estimated in a multi-unit deployment?

Per-unit cost is estimated by aggregating initial hardware, deployment, and integration costs with annual maintenance and any downtime-related losses. A disciplined model compares this figure to the productivity gains from automation over a multi-year horizon, enabling a defensible ROI assessment and a clear path to scale.

What uptime targets are realistic for multi-shift operations?

Realistic targets vary by task, but a practical benchmark is 90-95% uptime across 2-3 shifts with robust battery-swapping and predictive maintenance. Higher uptime consistently reduces per-task costs and improves fleet ROI, making the case for capital expenditure stronger over time.

When could a 30,000-unit plant influence procurement decisions?

Such a capacity milestone signals a trend rather than an immediate purchase order. It indicates a credible scaling path, where data on per-unit cost, uptime, and long-term maintenance become decisive for multi-plant rollouts, supplier negotiations, and financing terms.

What watchpoints should operators track before scaling?

Key indicators include publicly disclosed per-unit cost, verified uptime across shifts, transparent maintenance budgets, and a validated fleet-ROI model. Without these, scale decisions remain speculative; with them, the case for fleet deployment becomes data-driven and incremental.

Add a comment

To comment, you need to register and authorize

Comments

The broad labor shortage referenced in the discourse is a macro trend that invites the robotics narrative to step beyond a single plant and ask what the aggregates look like across an industry. If the capex bet can deliver higher uptime and lower per unit costs, the incentive to automate grows, but the social and economic ripples are substantial. A factory that adds hundreds or thousands of humanoid workers will still need humans in roles that design, maintain, and supervise the automation ecosystem. The real productivity gains come not from replacing every task, but from shifting task definitions, enabling workers to supervise larger fleets, focus on exception handling, and reconfigure lines with minimal downtime.

This perspective raises questions about how to pace training, safety, and change management. Workforce transitions require re-skilling programs, new career ladders for technicians, and clear channels for worker input into maintenance and upgrades. The deployment logic therefore overlaps with human resource strategy, industrial engineering, and even regional economic policy. If the industry converges on fleet scale, the demand for skilled technicians with robotics-savvy competencies could rise as much as the demand for more traditional manufacturing engineers.

From a capital markets view, the fifty thousand foot question is whether the price of reliability and the durability of the ROI will satisfy shareholders, lenders, and manufacturers who must compete with other capital priorities. The narrative suggests a credible trajectory where the model shifts from a bold R&D bet to a repeatable, scalable asset class. If this occurs, capital allocation could tilt toward platform bets—more robots, fewer one-off automation pilots—alongside a robust services ecosystem that maintains performance over time.

Finally, the regional and global implications deserve attention. Supply chain fragility, energy costs, labor mobility, and regulatory environments all color the economic calculus. A successful scaled deployment would create a blueprint for other sectors facing similar labor bottlenecks, while also prompting policymakers to consider incentives, safety standards, and workforce transition programs that align with a future where factory floors are powered by autonomously supervised fleets of intelligent assets.

The prudent operator view treats the ambition as a capital decision that will be resolved through data, not headlines. The near term milestones set expectations but do not guarantee results. The four practical watchpoints below summarize what must be visible before scale becomes sensible.

First, public per unit cost disclosure. The entire model rests on what a unit costs to acquire, maintain, and operate over its lifetime. Without an explicit price, ROI discussions risk devolving into optimistic scenario planning rather than disciplined budgeting. Operators should insist on a transparent breakdown of hardware, software, services, spare parts, and training, plus sensitivity analyses that show how ROI shifts with different labor costs.

Second, uptime and maintenance metrics. Reliability across multiple shifts and environments is essential. A credible plan should specify target downtime budgets, mean time between failures, and mean time to repair, along with a preventive maintenance schedule and the expected impact of battery swap cycles on availability. It should also outline the inventory levels for spare parts and the lead times to bring a replacement into service.

Third, total cost of ownership models. The deployment decision must compare the full asset lifetime costs to the savings from labor. This includes upfront capital, financing, installation, integration with existing lines, software updates, energy consumption, maintenance, and end-of-life considerations. The model should be robust to changes in the mix of tasks, product throughput, and the pace of other automation initiatives in the plant.

Fourth, fleet economics validation. A credible path from pilots to a scalable deployment depends on demonstrable data across a multi unit rollout, not a single line. Operators should demand staged milestones, published ROI criteria, and a governance process capable of updating the plan as new metrics arrive. The twenty twenty seven window will only produce credible signals if there is transparency about how the pilot results translate into a replicable production blueprint.

Additionally, there are wider risk dimensions to monitor. Supply chain stability, cyber security, and safety compliance can all influence the realized value of a humanoid fleet. Data governance concerns around collaborative research, including who controls the models and who benefits from the insights, deserve explicit consideration. Finally, the human dimension cannot be overlooked: the value of humanoid automation depends not only on numbers but on how workers are redeployed, upskilled, and integrated into a more productive ecosystem.

Taken together, these watchpoints turn a headline figure into a decision framework. The math is not settled, but a disciplined, data-driven approach can reveal whether the desert of uncertainty still hides a viable oasis of cost savings, or whether the deltas in timing and cost make the thirty thousand unit dream a staging ground for further pilots rather than a blueprint for scale.

In the near term, success will be measured by integration: how well the Atlas platform communicates with existing lines, how robust the robot is to the environment, and how predictable the end-to-end workflow becomes. The lack of a confirmed price means procurement teams must work with scenario analysis, but the story implies that meaningful price signals will emerge in the next wave of deployments. The practical takeaway for operators is to evaluate not just the robot's skill but the total package: the software, the services, the integration, and the potential vendor support across shifts.

Two diagnostic contrasts emerge. One, the thirty thousand unit goal is a capex bet on labor replacement through scale rather than a turnkey labor swap in the near term. Two, the verticalization of a humanoid supplier into hardware, software, and services reframes the problem away from a pure software feasibility exercise to a factory floor uptime and maintenance challenge. Operators should therefore demand clear criteria for price visibility, long term reliability, and TCO across an entire plant portfolio, not just a prototype line.

The bottom line is that even at full scale, this ambition remains a relative move against a large labor gap. The key question for buyers is whether per unit costs and uptime trends improve enough to justify committing capital and reconfiguring the plant for a fleet of robots. If the numbers begin to cohere, the plant could become a credible productivity lever in the hands of a broader base of manufacturers; if they do not, the episode risks becoming another headline about what could have been if conditions were perfect.

Two anchors help frame the current economics. First, uptime matters because value erodes when a unit is offline. The battery swap capability is not a gimmick; it is a mechanism to extend multi shift operation and reduce the need for manual intervention. Its effectiveness will determine the required spare-parts inventory, the pace of maintenance, and the scale of the fleet that a factory can support. Second, the absence of public per unit pricing creates a degree of uncertainty. Yet the story suggests that improvements in uptime and faster changeovers could meaningfully compress the total cost of ownership, making large fleet deployments plausible even if initial unit prices are high.

The piece distinguishes pilots from deployment. For operators, the critical shift is from asking if Atlas can do a task to whether a fleet of Atlas units can deliver measurable productivity advantages at a credible cost. The plant is presented as a cost and reliability play, not a spectacle of robotic finesse. If the economics hold, this could reframe procurement toward capacity commitments and multi facility rollouts rather than single demonstrations. If not, it invites caution about conflating aspiration with near term reality.

In sum, progress should be measured in tangible metrics: uptime, maintenance cost, and, above all, a transparent comparison of fleet economics against the cost of human labor across an operating year. Only with those signals can the capex bet be judged as a prudent strategic move or as a misread of the value of robotics in manufacturing.